How Much Do You Need to Start an Etrade Account

How much money does it take to start an IRA?The easy answer is $0, but that won't get you on your way to growing your money into retirement. The truth is, you can start an IRA with very little money. The keys to really take advantage of the power of Roth IRAs or Traditional IRAs are to understand your eligibility, the rules, and to consistently add to your account over time.

IRA's are easy to start. Just open up a great online brokerage account. My personal favorite right now is M1 Finance.

Keep in mind that there are actually two main types of IRAs to consider, so make sure you understand which one you are eligible for.

Table of Contents

- Which IRA Am I Eligible For?

- How Much Money Does it Take to Start an IRA?

- How to Start Investing in an IRA

- Know the IRA Rules

- Summary

Which IRA Am I Eligible For?

Virtually anyone can contribute to an IRA, Roth or traditional. The most basic requirement is that you haveearned income.The difference between the two is based on when you'll pay taxes.

A traditional IRA allows you to grow your money tax-free over time. You won't pay income taxes on your account until you begin taking distributions in retirement age, or when you're at least 591/2. You may be able to deduct your contributions on your taxes if you meet specific filing status and income requirements.

With a Roth IRA, on the other hand, you'll contribute income that has already been taxed, so you don't get a tax deduction right off the bat. Your money will grow tax-free, however, and you won't have to pay income taxes on your account once you begin taking distributions in retirement.

Here is a tool to help figure out what type of IRA you're eligible for:

| Traditional IRA | Roth IRA | |

| Contribution Limits | $6,000 total across all IRAs in 2020; if you're ages 50 and older, you can contribute an additional $1,000 | $6,000 total across all IRAs in 2020; if you're ages 50 and older, you can contribute an additional $1,000 |

| Who Can Contribute? | Anyone who earns an income and is under the age of 70 1/2 | Anyone who earns an income |

| Do Income Caps Apply? | Income caps limit who can deduct contributions on their taxes unless you don't have a retirement plan through work | Income caps limit who can contribute |

| How Do Taxes Work? | You'll pay taxes on distributions once you begin taking them in retirement | Your distributions will be tax-free once you reach retirement age |

| Who Is This Account Best For? | Anyone who can deduct contributions and wants to reduce their taxable income | Someone who wants tax-free income in retirement |

Heads Up: no matter which type of IRA you choose (or if you contribute to both), you'll face an IRA contribution limit for each tax year. In 2020, you can contribute up to $6,000 in total to an IRA if you're under the age of 50. If you're 50 or older, the limit is $7,000.

How Much Money Does it Take to Start an IRA?

Now you know what type of account to open, so how much do you invest? Technically, you don't need anything to open an IRA since the Internal Revenue Service (IRS) doesn't set minimum contribution limits — only annual maximums. However, individual brokerage firms have minimum requirements and you want to employ a healthy contribution strategy to maximize rewards.

When it comes to your contributions, remember that the important thing is to just get started. Small amounts of money can add up over time, and from there, compound interest can do its magic and help your account balance balloon. Here's one way to think about it:

| Monthly Contribution | Annual Contribution |

| $5 | $60 |

| $10 | $120 |

| $25 | $300 |

| $50 | $600 |

| $100 | $1,200 |

| $200 | $2,400 |

| $500 | $6,000 |

Let's say you're 30 years old, and you contribute $100/month for a total of $1,200 a year to your Roth IRA. By the time you're 67 and ready to retire, you'll have saved $204,000 that won't be subject to income taxes. That can go a long way to support a happy retirement.

Now that you understand the process a bit more, figure out which brokerage firm to use for your IRA, and how much you need to actually open an account and get the ball rolling. Once your account is up and running, you can figure out how much to contribute regularly, whether that's $100 per month or $100 per week.

How to Start Investing in an IRA

1. Compare online brokerage firms that offer IRA accounts

Different online brokerage firms have features that you'll want to pay attention to. Some are better for hands-off investing, while others are better for those who want to get their hands dirty and really dig in.

Here are some of the things you should ask yourself when choosing a brokerage:

- Would you rather be hands-on or hands-off with your account? A robo-advisor may take the burden off you when it comes to managing your investments.

- What sort of investments do you want to buy? Pay attention to limitations with the broker.

- How much are you looking to invest off the bat? Fees and commissions can eat away at early earnings if the initial investment is too small.

Here are some of our favorite options:

![]()

- $0 per trade

- $0 set up / $100 invest

- $0 annual

![]()

- $0 per trade

- $0 mutual fund

- $0 set up

- 0.25%-0.40% account balance annually

![]()

- $0 per trade

- $9.95 mutual fund

- $0 set up

- $0 annual

Among the best brokerage accounts for beginners, we like M1 Finance for IRAs. You only need $100 to open an account with M1 Finance, which is a threshold most beginning investors can reach. M1 Finance IRAs also come with no hidden fees, the option to invest in fractional shares, and a helpful mobile app that lets you monitor your account growth no matter where you are.

2. Fund your account

Now it's time to put the minimum amount in to fund your brand new account. As previously mentioned, different brokerages have different minimum requirements, so

3. Select your investment strategy

Your next step is building a system that will allow you to seamlessly build wealth over time. This means figuring out how much you can afford to invest in an IRA each month, but it also means choosing investments that will exist within your IRA.

Remember: Your IRA is nothing more than a retirement vehicle you can use to save and invest for the future. Once you open an IRA, you still have to choose the investments that do the work inside your account.

If you find you are able to deduct contributions to a traditional IRA because your employer doesn't offer a retirement plan, you should strive to contribute as much as you can each month up to the $500 monthly (and $6,000 annual) limit. That way, you're building up retirement funds in a hurry while maximizing tax advantages. If you opt for a Roth IRA instead, you won't get any tax advantages now, but you will later on since you won't have to pay income taxes on distributions once you reach retirement age. Either way, the ultimate goal is striving to invest as much as you can each month up to account limits, and without harming your other financial goals.

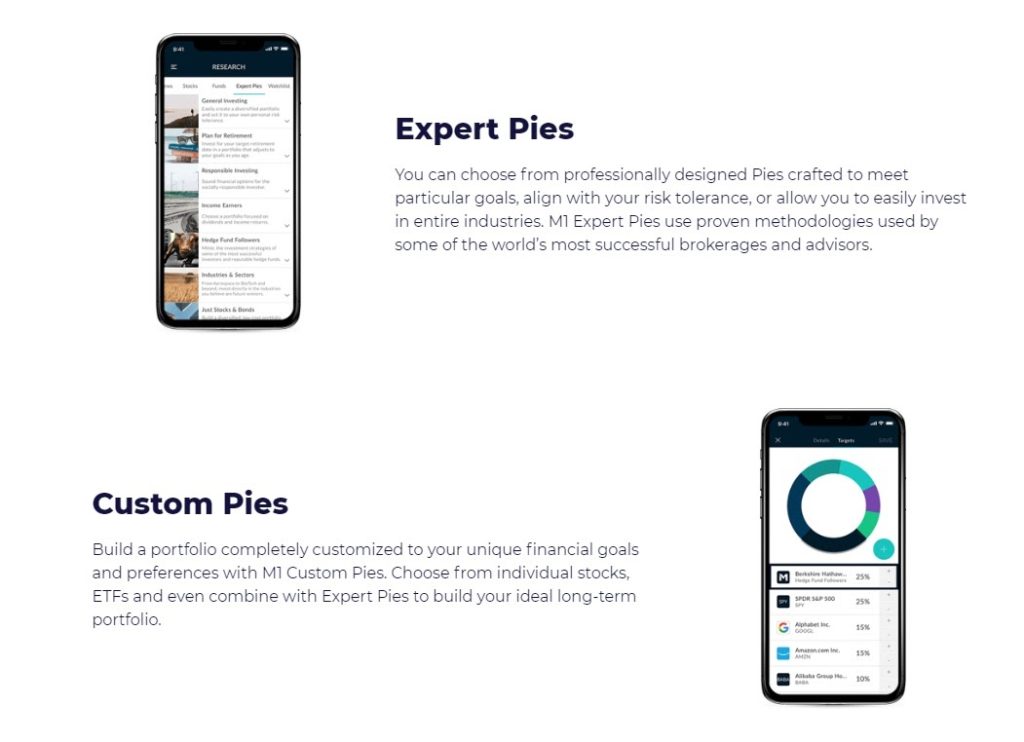

In terms of selecting your portfolio, this component of your system depends a lot on which investment platform (brokerage firm) you choose to go with. Some firms like M1 Finance let you set up "pies" of investments that are based on fractional shares. With M1 Finance, you can build your own "pie" from more than 6,000 available stocks and funds, but you can also choose from "Expert Pies" that have been put together by in-house investment professionals.

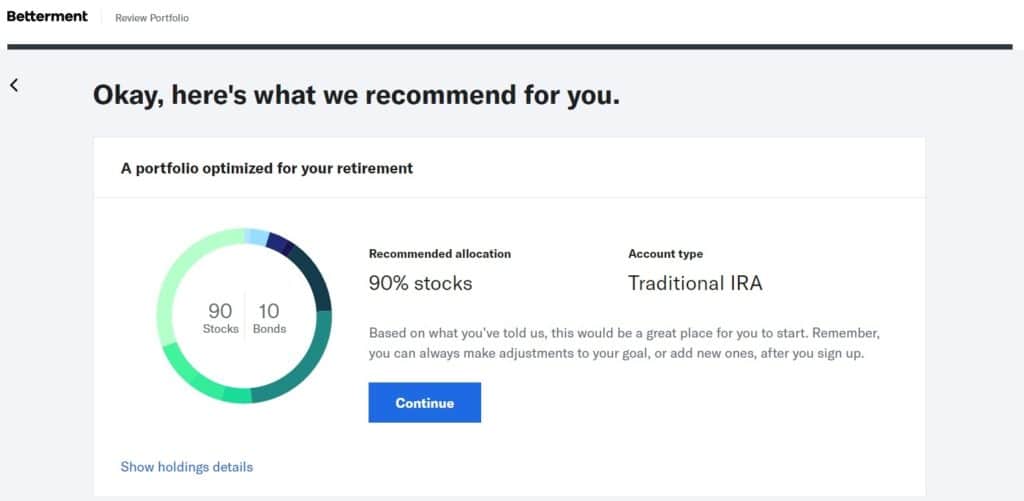

That's just one way this can work, but there are plenty of other ways to set up a portfolio depending on the firm you choose. For example, let's imagine you decide to open an IRA with Betterment.

Betterment is a robo-advisor that helps you formulate an investment plan based on your age, your investing goals, and your risk tolerance. As a result, opening an IRA with Betterment is a breeze. You'll start by answering some basic questions about yourself, including your age, your income, and when you plan to retire. From there, Betterment will suggest a specific investment plan that is formulated to help you achieve your goals.

If you're a knowledgeable investor who wants to select the stocks, bonds, ETFs, and other investments that live within your IRA, that's perfectly okay, too. Just remember that some brokerage firms will help create an investing plan for you based on how much you can invest and your long-term goals.

4. Make it automatic

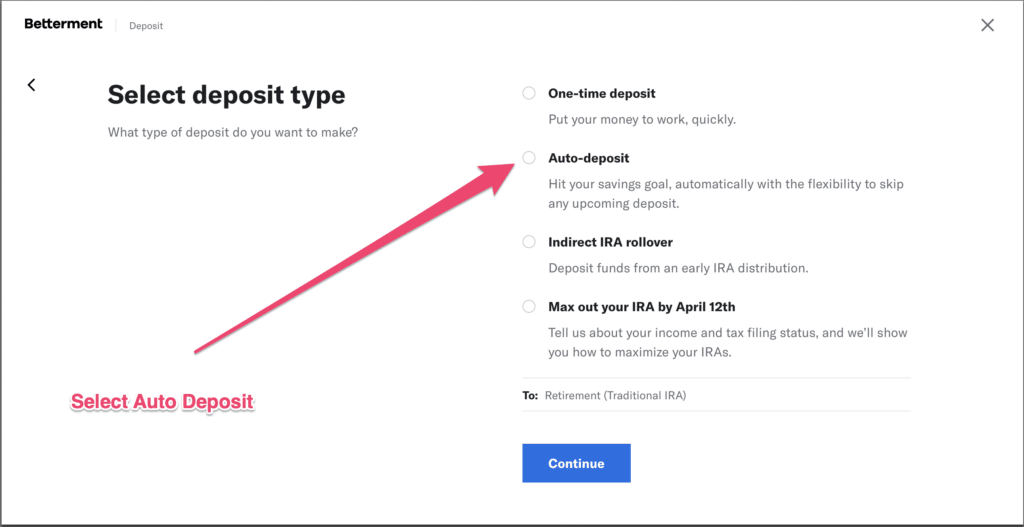

To help in your effort to contribute consistently, and to remove some of the pressure, consider making your investments automatic with the click of a button. Many of the top brokerage firms let you set up automatic investments through their mobile apps or online platforms, including Betterment's example below.

5. Check in regularly and stay on track

Part of the fun of putting away money for your future is watching it grow. Keep an eye on your portfolio to make sure you're contributing the way you want to. It can be tempting during tighter financial times to stop contributing, but you can always reduce your contribution amount depending on your circumstances and then change it back later. Don't worry about small fluctuations and seek help from an advisor if necessary.

Know the IRA Rules

Whether you opt for a traditional IRA or a Roth IRA, you should know that plenty of rules dictate who can contribute, how much can be contributed each year, and whether contributions are tax-deductible.

With a Roth IRA, the rules are as follows:

- Roth IRA contributions are made with after-tax dollars, so they are not tax-deductible.

- Your money will grow tax-free until you reach retirement age, and you won't pay income taxes on your distributions when you retire.

- You can remove contributions to your Roth IRA from your account at any time before age 59 1/2, but you cannot take out any earnings without a penalty until then.

- Married couples filing jointly can contribute the full amount to a Roth IRA provided their modified adjusted gross income (MAGI) is below $196,000. Those with incomes between $196,000 and $205,999 can contribute a reduced amount. Those with incomes over $206,000 cannot contribute.

- Single tax filers can contribute the full amount to a Roth IRA provided their modified adjusted gross income (MAGI) is below $124,000. Those with incomes between $124,000 and $138,999 can contribute a reduced amount. Those with incomes over $139,000 cannot contribute.

With a traditional IRA, the rules are as follows:

- Money invested in a traditional IRA grows tax-free. However, you will pay income taxes on distributions once you reach retirement age.

- If you are covered by a retirement plan at work and you're single, you can deduct contributions to a traditional IRA if your MAGI is below $65,000. You can claim a partial deduction if your MAGI is between $65,000 and $74,999. For those with incomes over that amount, contributions cannot be deducted on your taxes.

- If you are covered by a retirement plan at work and you're married filing jointly, you can deduct contributions to a traditional IRA if your MAGI is below $104,000. You can claim a partial deduction if your MAGI is between $104,000 and $123,999. For those with incomes over that amount, contributions cannot be deducted on your taxes.

- If you are single and don't have a retirement plan at work, you can deduct the full amount of your contributions to a traditional IRA regardless of your income.

- If you're married filing jointly and your spouse is covered by a retirement plan at work but you're not, you can deduct the full amount if your MAGI is below $196,000. Those with MAGIs between $196,000 and $205,999 can deduct a reduced amount. Anyone with a MAGI of $206,000 or higher cannot deduct IRA contributions on their taxes.

And, as we mentioned already, both accounts come with an annual contribution limit of $6,000 for 2020. If you're 50 or older, you can contribute an additional $1,000 for a total of $7,000.

Summary

Opening an IRA is a great way to save more money for retirement and the future, and that's true whether you opt for a traditional IRA or a Roth IRA. Just remember that each type of IRA has pros and cons, and you'll need to consider your tax situation now and what it might look like later.

Still, you shouldn't get so caught up in the rules and minutiae of these accounts that you fail to open one altogether. Do some basic research then decide which brokerage firm will meet your needs the best. From there, open an account and start contributing as much as you can. The rest of the details will work themselves out, but only if you get started.

How Much Do You Need to Start an Etrade Account

Source: https://www.goodfinancialcents.com/how-much-money-do-you-need-start-roth-traditional-ira/

0 Response to "How Much Do You Need to Start an Etrade Account"

Post a Comment